CYCLE TIMING ANALYSIS (by Intraday Dynamics)

The premise of this update is to question whether we are about to see a potential shift in equities in the coming 2-3 months.

Since early November, market sentiment has been a yo-yo with rampant buying following the election by both funds and retail investors. Following the December FOMC meeting, funds have been net sellers of the market while retail investors have continued to pile in to high flying tech stocks and meme coins.

The reality is February is ushering in a period of potential volatility in stocks. This runs through the first week of May 2025.

Granted, there remains a deep bullish sentiment calling for a vertical in stocks and that is certainly not off the table.

That said, the past three weeks we have included a section of charts under the heading Warning Signs? in the weekly update that illustrate some of the troublesome data points in this market.

When it comes to potential trend changes, the key is to survey the horizon for events that might offer signals that things could be shifting.

The first of these came in mid-December 2024 when the Fed took a more hawkish stance on rates. Since that period, we have had one impulse day where the Dow was off 1123 points and funds became net sellers.

The second of these is the inauguration of 20 January 2025 where retail traders began to be much more aggressive in their purchases of stocks with a focus primarily on the MAG7.

The third was the past week’s announcement of DeepSeek AI, which was quickly dismissed as an overreaction by the markets…without really digging into the data. As was pointed out in Friday’s update, some quants have shown that DeepSeek is a “Disinformation Machine.”

The fourth is the beginning of tariffs and potential trade wars. This comes at a time when trade balance numbers are already into new lows as consumers front-ran the tariffs with large trade in November and December. Plus, there’s already betting markets on how soon the tariffs will be pulled down…anywhere from 2-3 days to 4-5 months.

How does all this map out with the timing?

The month of February has potential to see a shift in market sentiment which will likely kick off with the U.S. Employment data on Friday.

There will be multiple critical cycle dates hitting, starting with 6-7 February 2015, with 19 February 2025 pointing to a place where fast moves can occur. The dates map out as thus:

- 02/06-07 *** X critical

- 02/19 *** X critical (fast moves)

- 02/24 **

- 03/03 ***

- 03/11-12 *** X critical

- 03/21 *** X

- 03/27-28 *** X critical

- 04/07 **

- 04/12 **

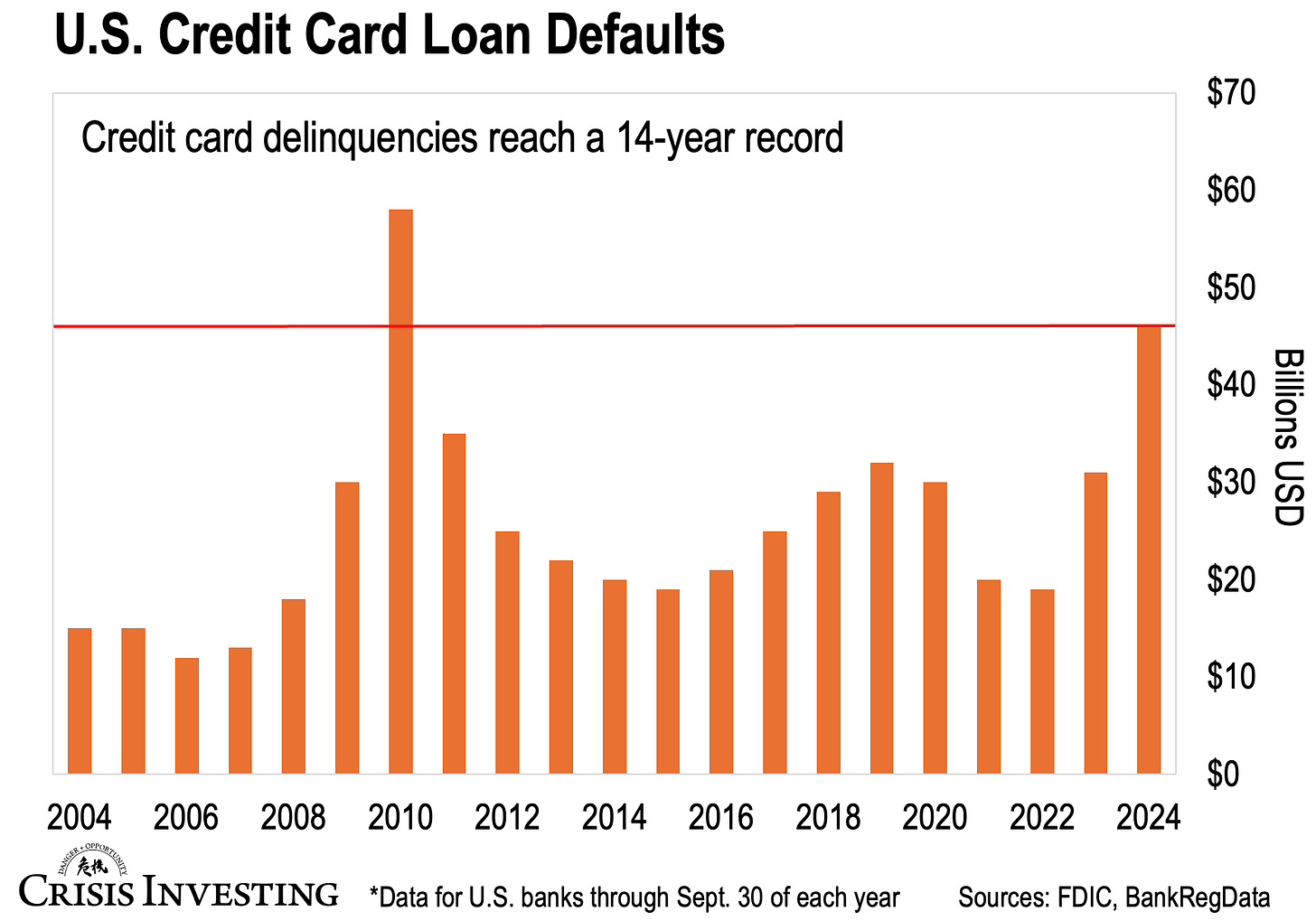

Now, as far as bullish/bearish potential. The funds have started to take some larger bets on the downside recently. They can see the retail enthusiasm flooding the market while consumers are sitting on $1.17T in debt with 23% interest and a 14-year default rate, and we all know that there are any number of shaky conditions not the least of which is the massive debt balloon that has been pumping this market for a decade.

Here are just a few of the warning signs that might make February a rough month for equities.

Warning Signs?

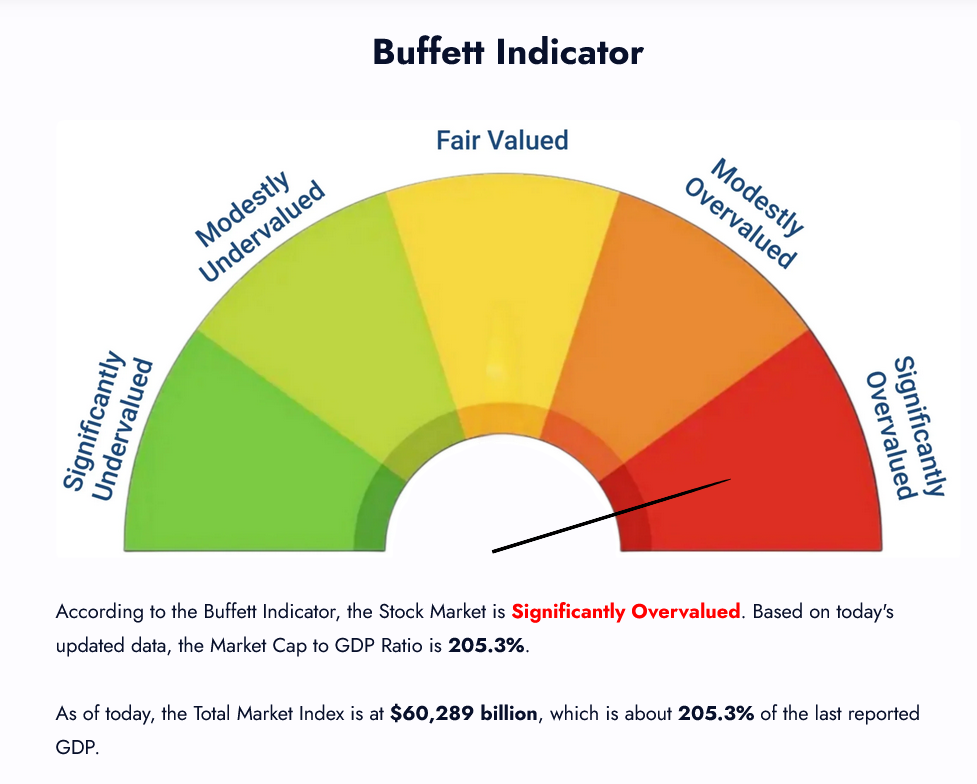

The “Buffet Indicator” remains at a record high of +202%+ of GDP. Previously, we talked about Berkshire having the largest cash reserves on record.

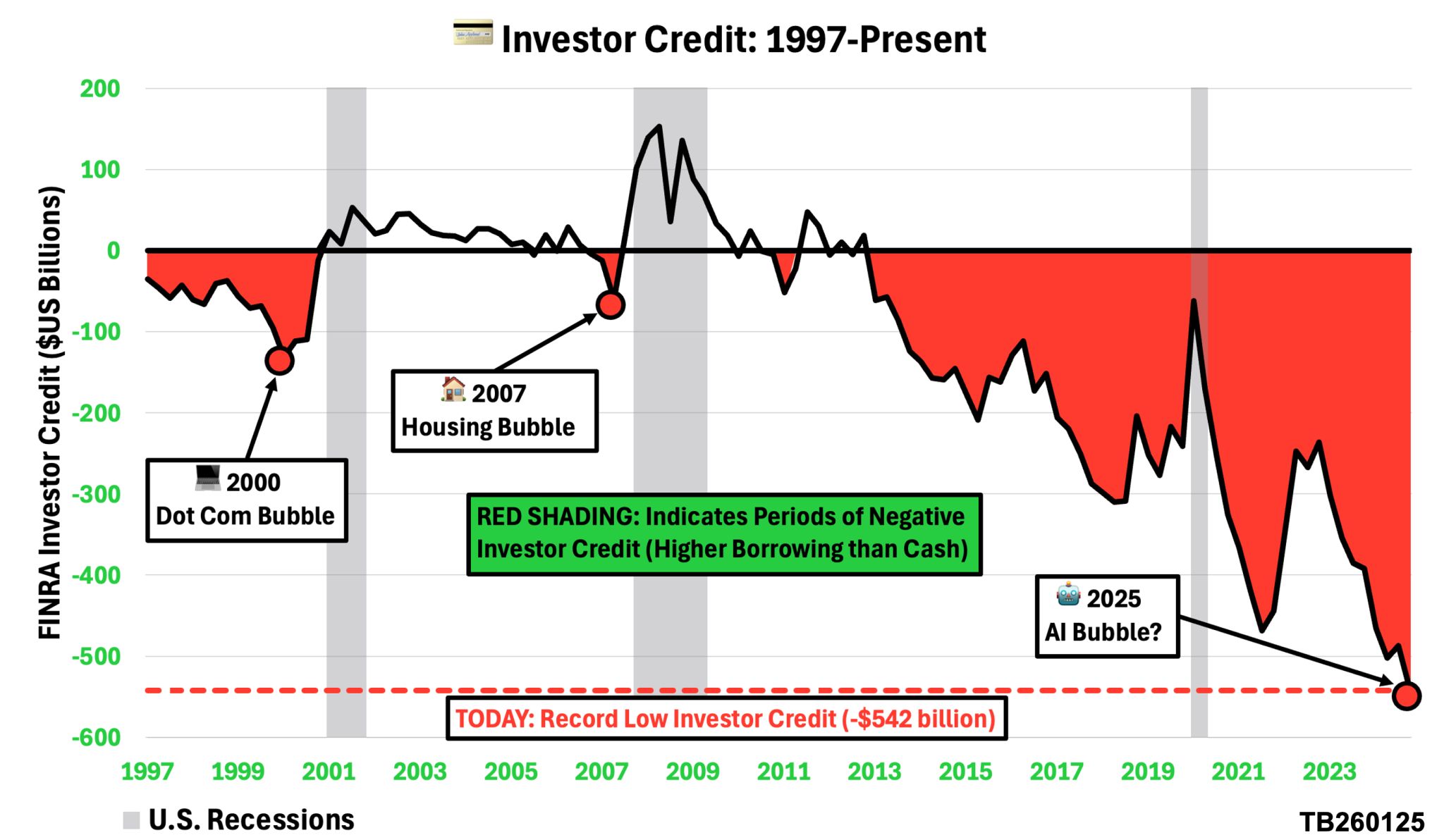

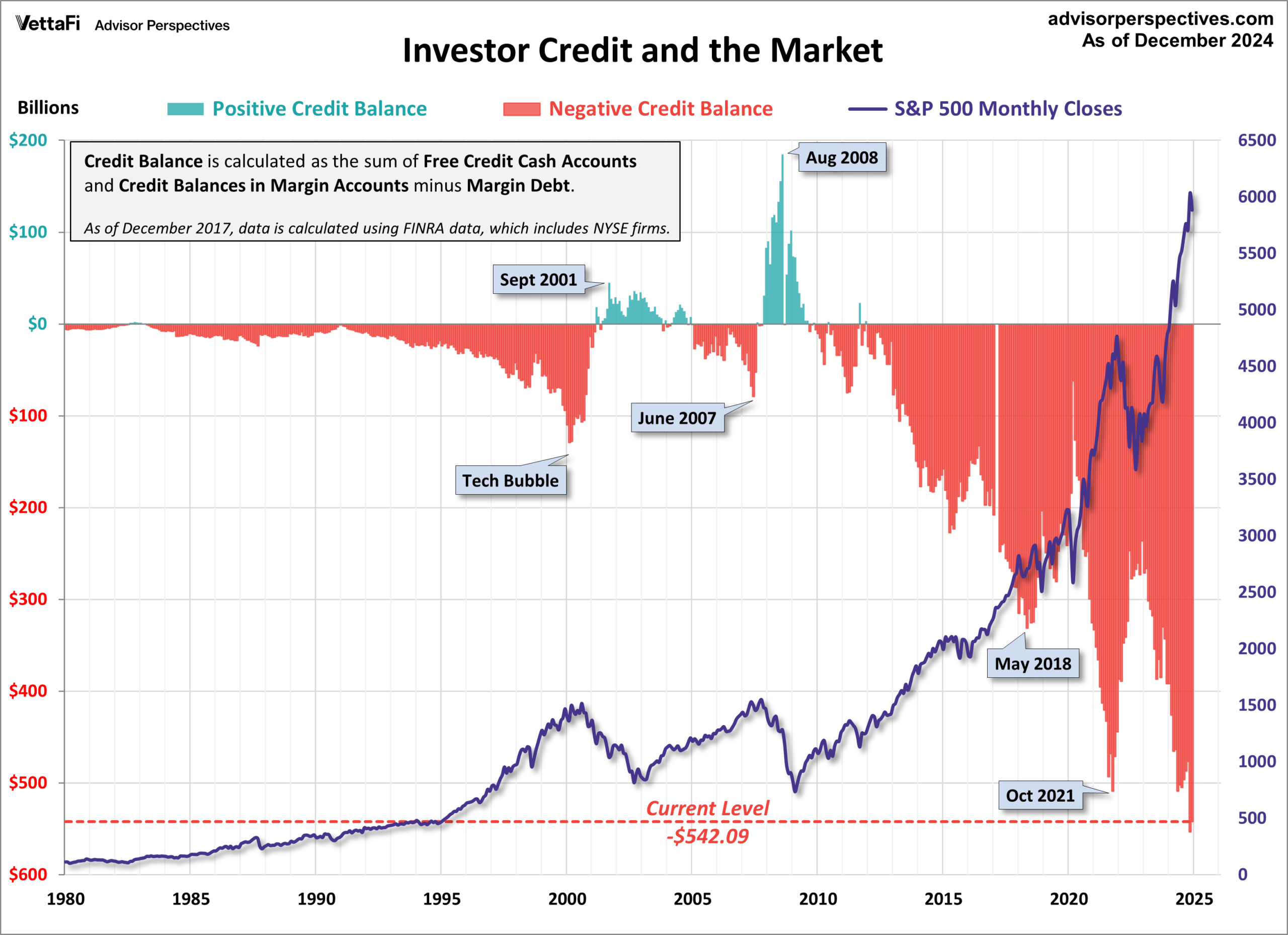

The market has been fueled by massive amounts of debt. How long can this massive negative Investor Credit binge continue? Can this go on forever?

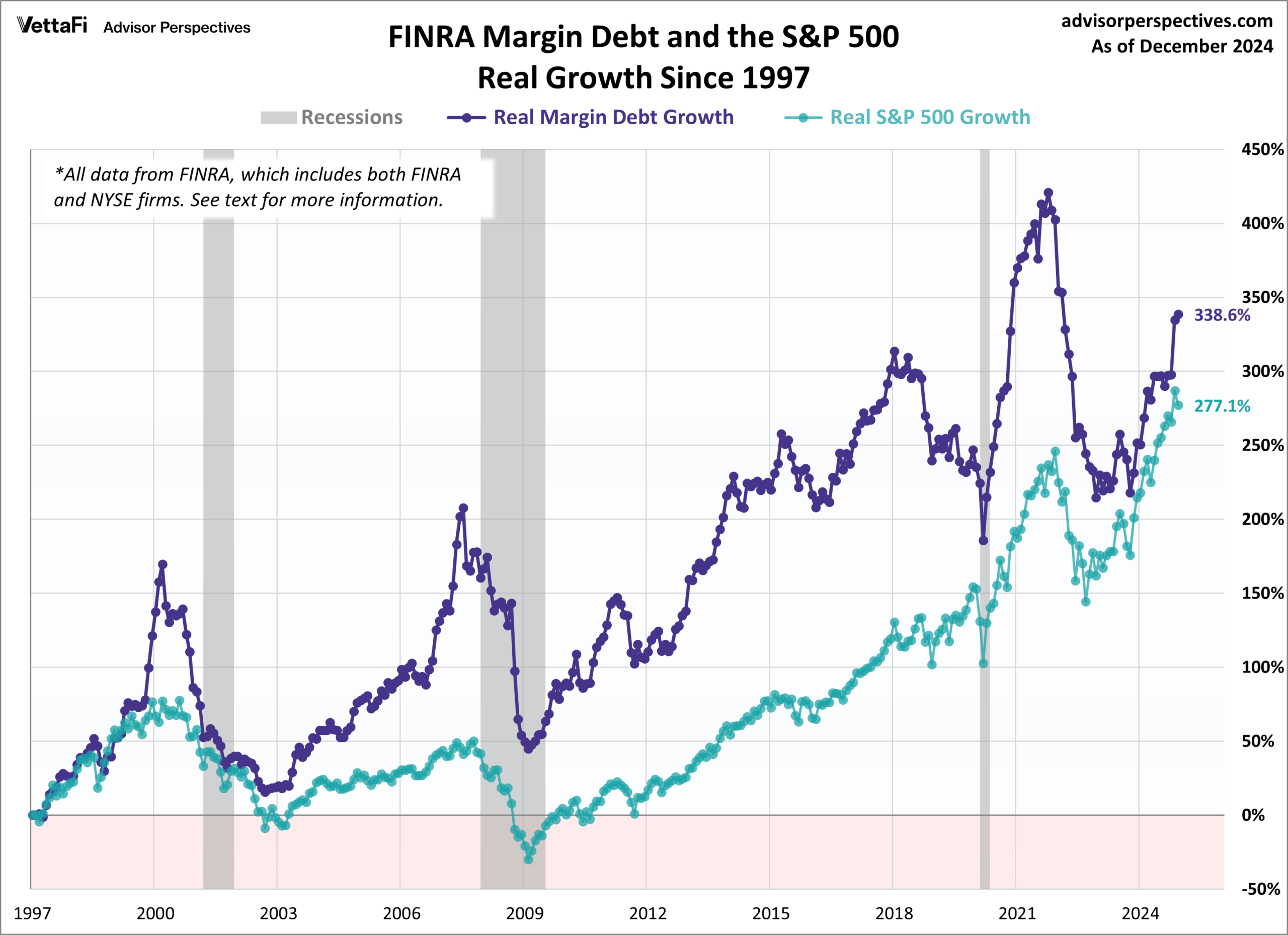

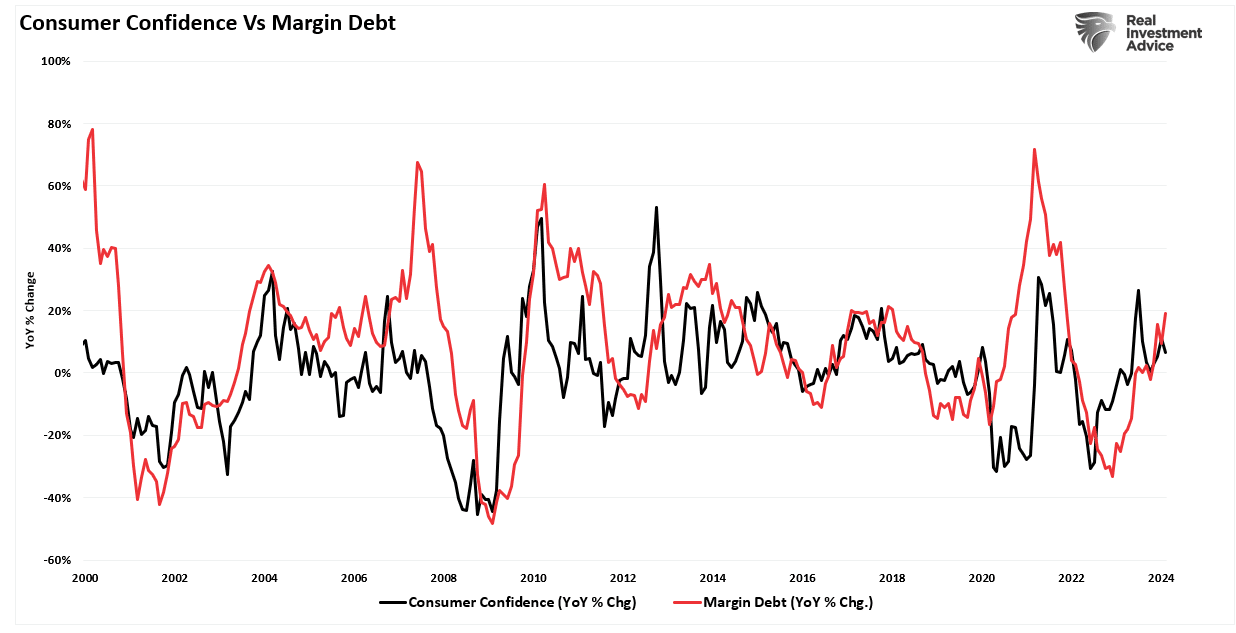

Margin debt has started soaring again. Weak hands? This is happening while consumer confidence is flat lining.

Margin debt has started soaring again. Weak hands? This is happening while consumer confidence is flat lining.

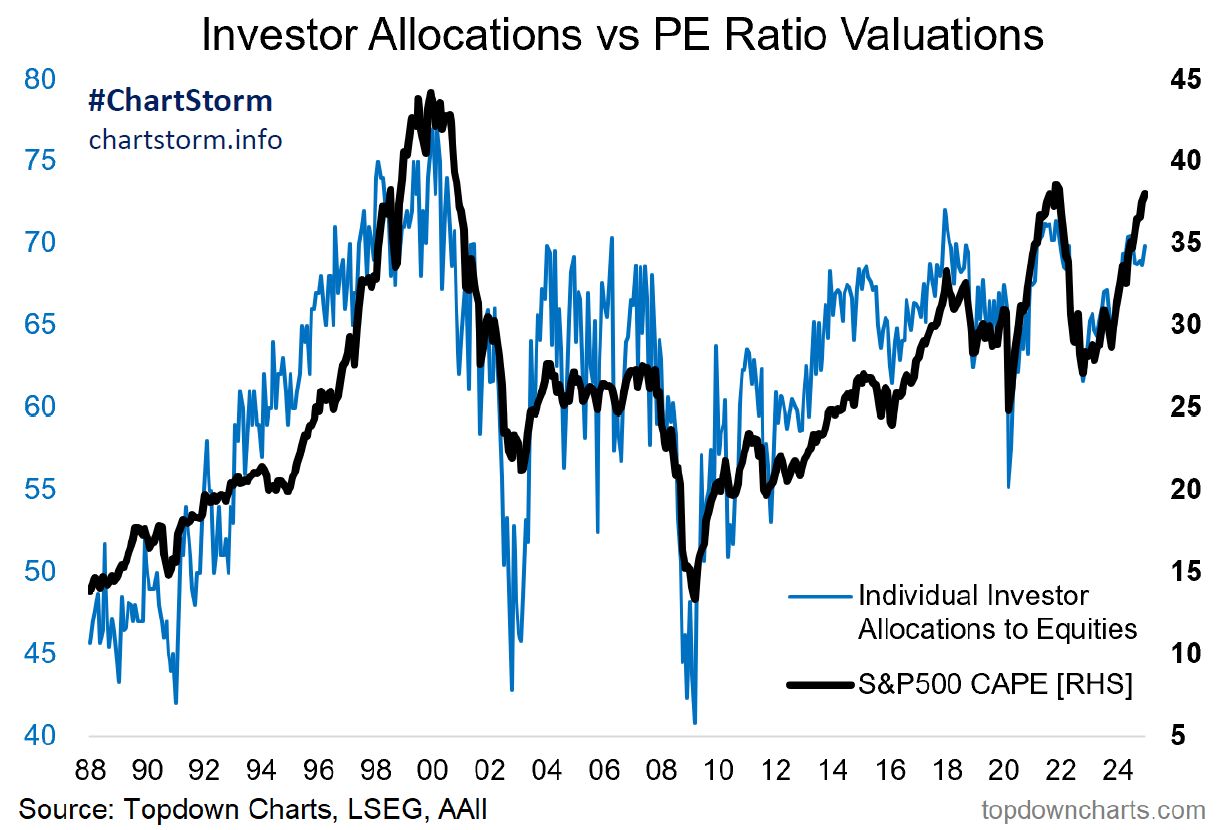

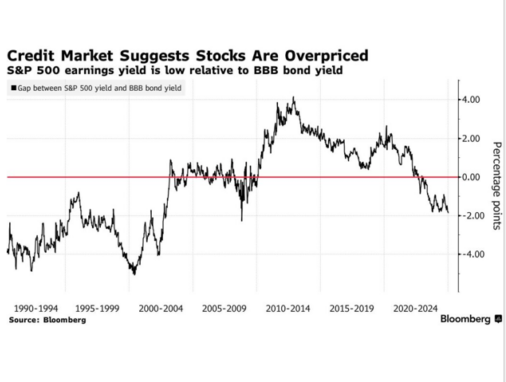

Valuations are stretched.

Valuations are stretched.

Equity funding spreads have collapsed since mid-December (managed funds are selling).

Equity funding spreads have collapsed since mid-December (managed funds are selling).

The market is gobbling up debt in a vertical. Where is the fuel going to come from to keep feeding this monster?

The market is gobbling up debt in a vertical. Where is the fuel going to come from to keep feeding this monster?

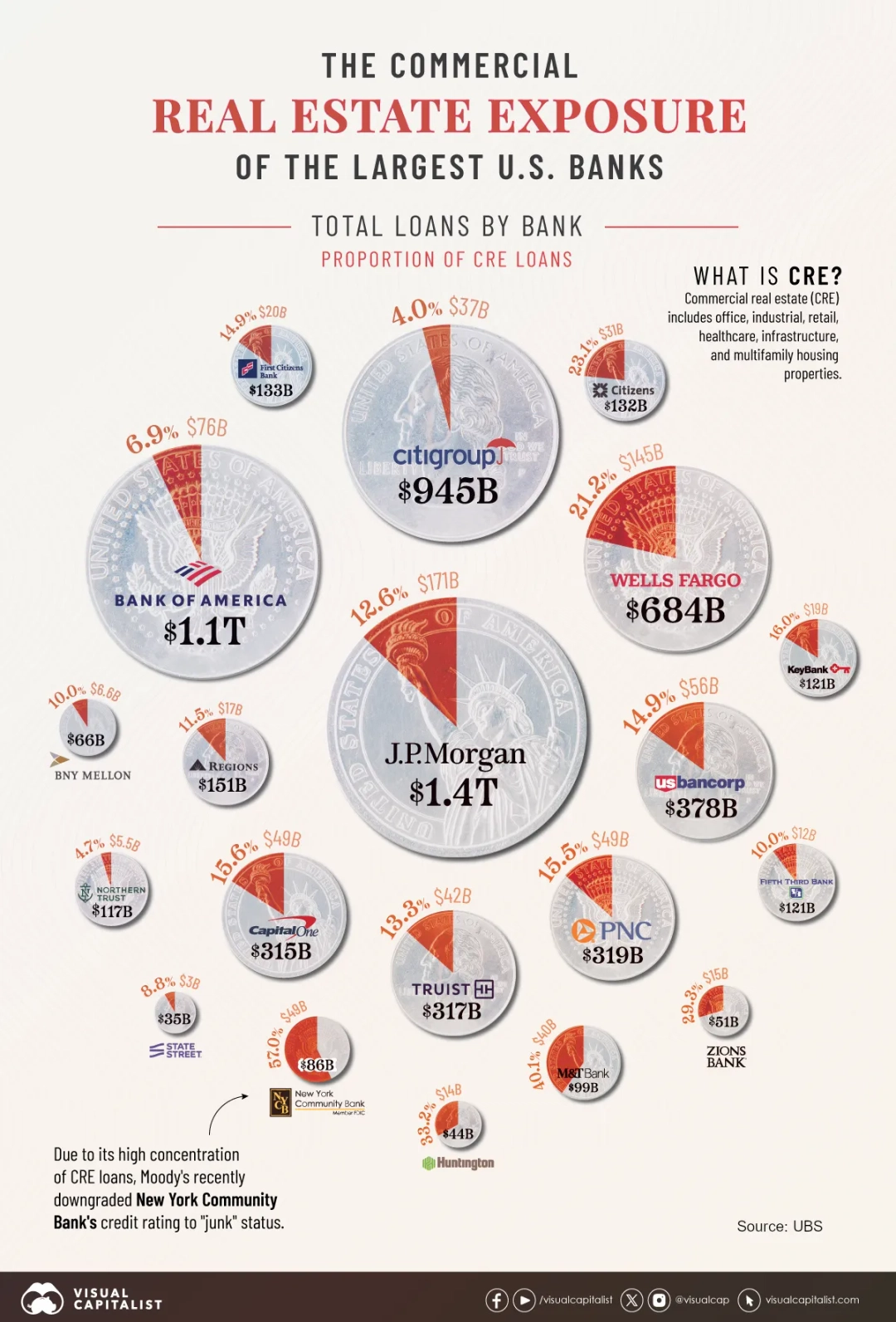

Commercial real estate is sketchy with barely 50% occupancy and banks sitting on toxic loans on the buildings. This is a global phenomenon.

Commercial real estate is sketchy with barely 50% occupancy and banks sitting on toxic loans on the buildings. This is a global phenomenon.

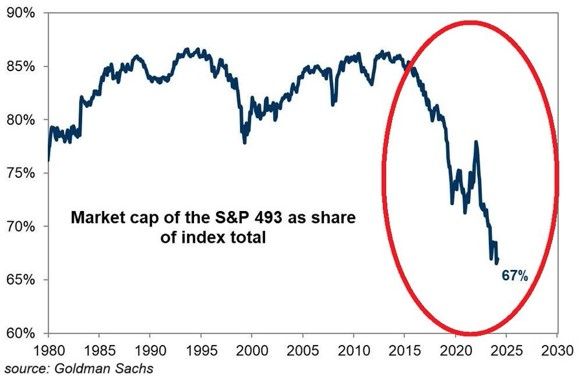

The S&P 500 bottom 493 stocks only account for 67 percent of the index now, with all the “pump” in the Magnificent Seven.

The S&P 500 bottom 493 stocks only account for 67 percent of the index now, with all the “pump” in the Magnificent Seven.

Options have become a massive portion of everyday trade in the stock market. This smells of a casino-like atmosphere.

Options have become a massive portion of everyday trade in the stock market. This smells of a casino-like atmosphere.

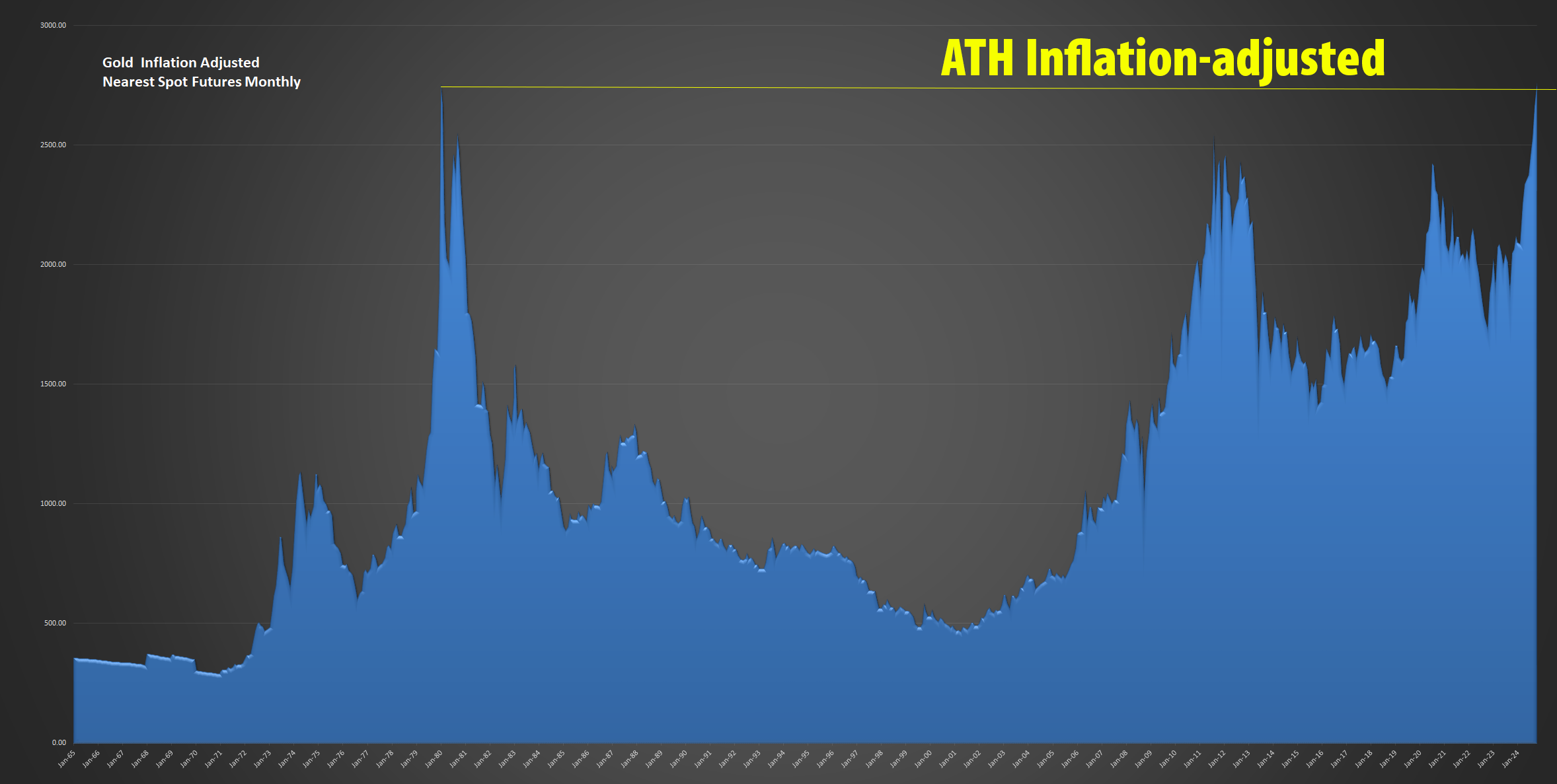

Central banks have been on a buying spree for gold and this past month spot gold futures set a new record high on the inflation-adjusted chart.

Central banks have been on a buying spree for gold and this past month spot gold futures set a new record high on the inflation-adjusted chart.

John Williams Shadow Stats show inflation substantially stickier than what the Central Banks suggest. (Dated chart)

John Williams Shadow Stats show inflation substantially stickier than what the Central Banks suggest. (Dated chart)

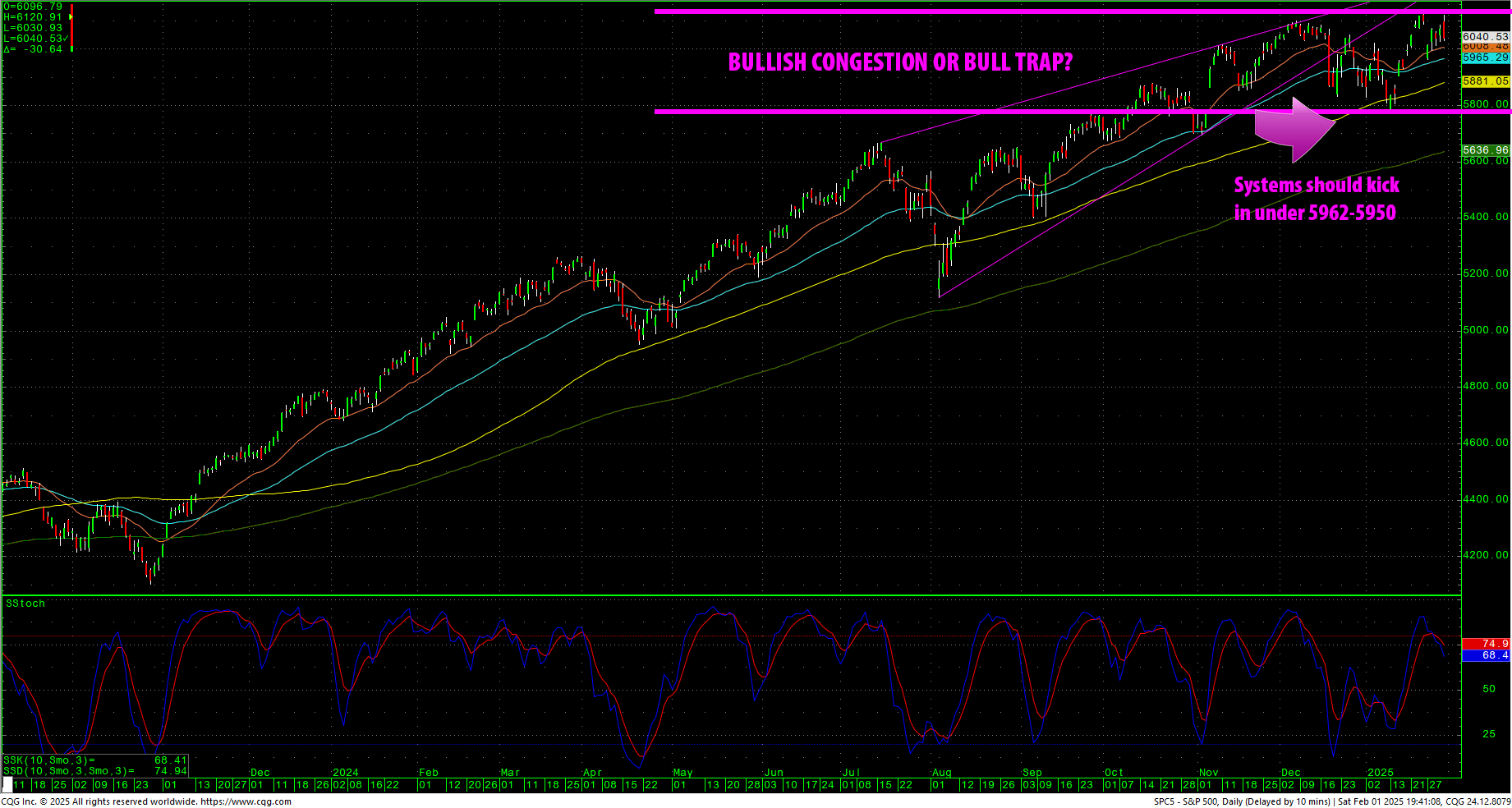

The S&P is in a roughly 200-point range that is either congestion or a massive bull trap. Computer systems should kick in hard under 5962/5950.

The S&P is in a roughly 200-point range that is either congestion or a massive bull trap. Computer systems should kick in hard under 5962/5950.

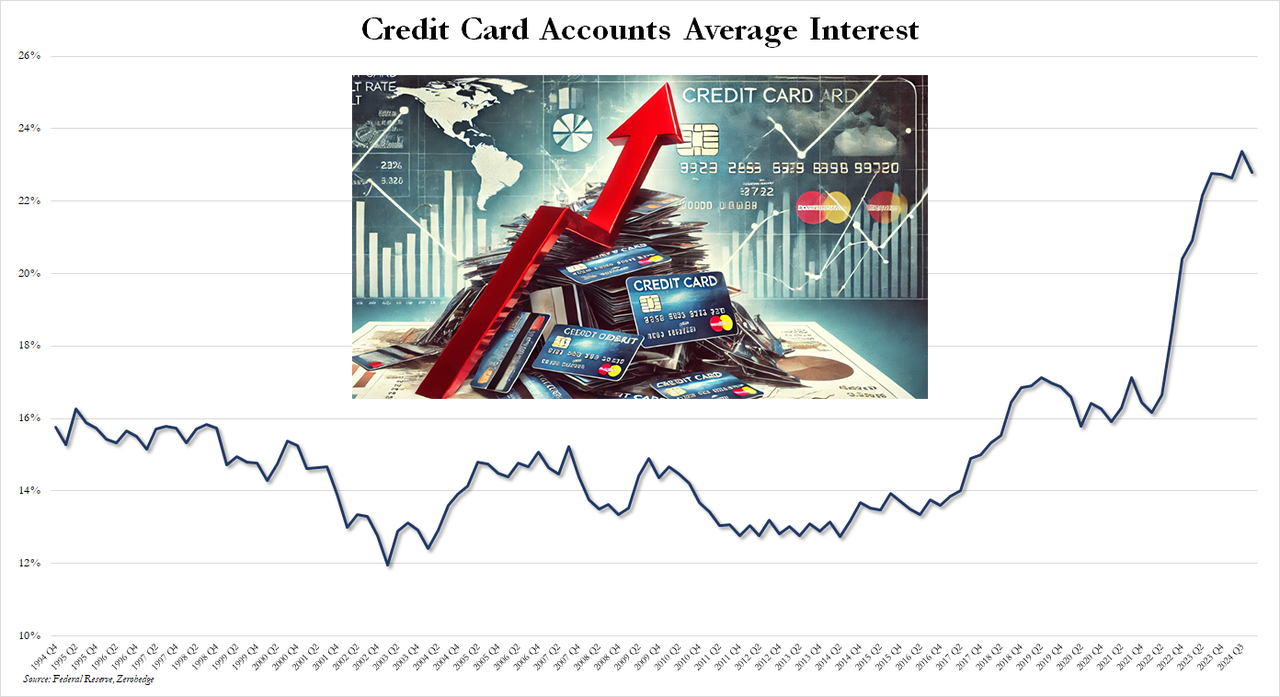

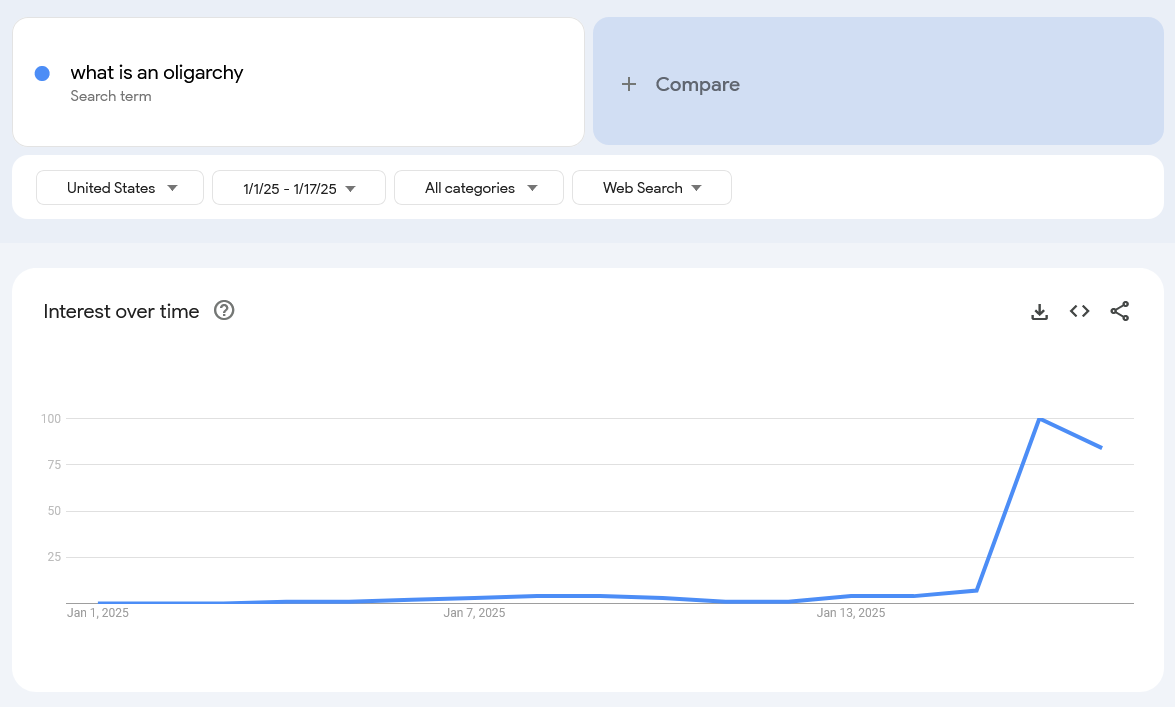

The market lives off debt. Consumer debt has reached $1.17 trillion while consumer credits defaults have reached a fourteen-year high. Consumer Revolving Credit was off sharply in late 2024. Consumer credit card rates have hit 23%. Consumers are maxed out. At the same time, consumers only just this week started asking Google, “What is an oligarchy.”

The market lives off debt. Consumer debt has reached $1.17 trillion while consumer credits defaults have reached a fourteen-year high. Consumer Revolving Credit was off sharply in late 2024. Consumer credit card rates have hit 23%. Consumers are maxed out. At the same time, consumers only just this week started asking Google, “What is an oligarchy.”

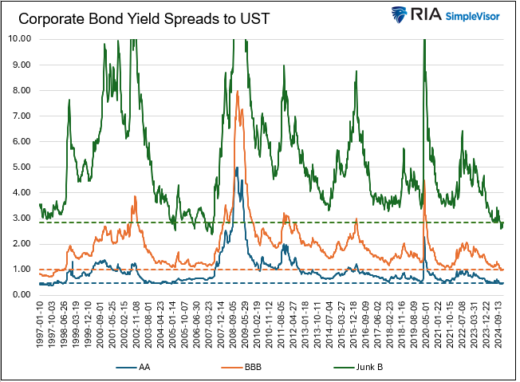

Corporate bonds and credit markets are flashing signs as well.

Corporate bonds and credit markets are flashing signs as well.

You Be the Judge

You Be the Judge

{kind=link}

The funds could be wrong and their recent selling into retail hands may backfire. The Fed may come o the rescye again with QE (inflation). That said, the critical timing starting this month may signal a shift in the charts and overall thinking about the intermediate-term health of the market.

Again, the timing runs through the first week of May and timing will be updated to reflect this in the weekly updates.